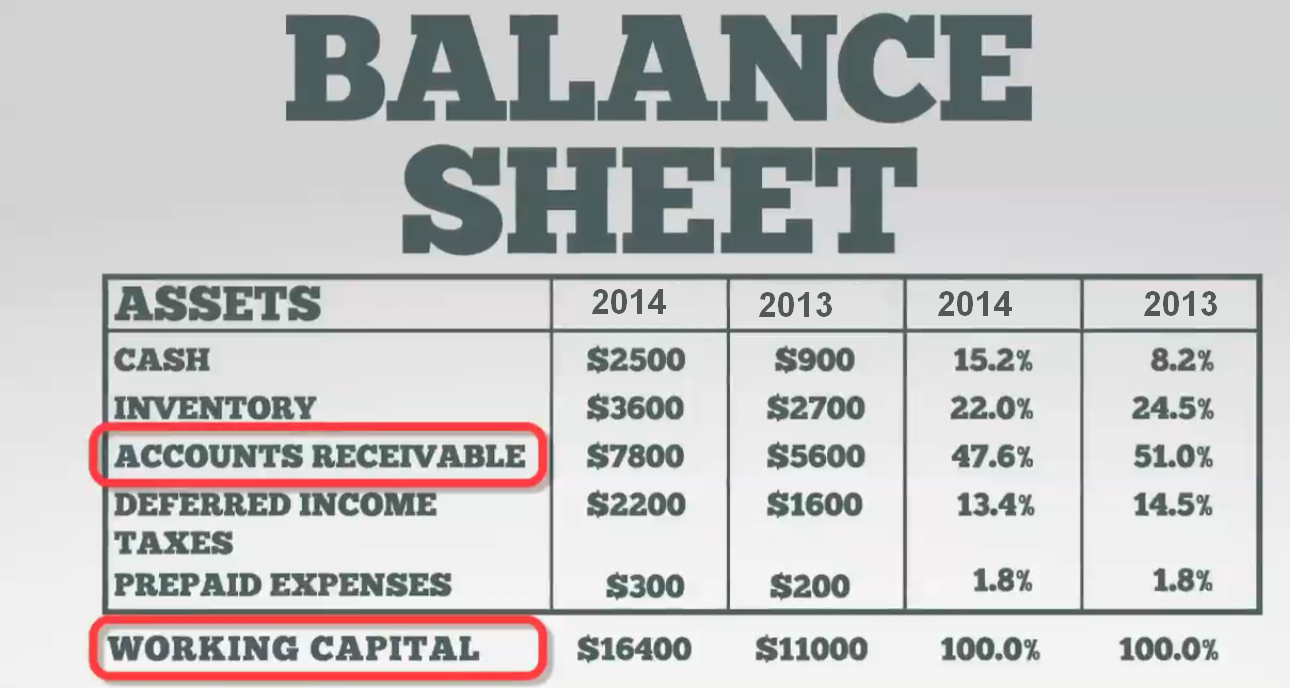

In balance sheet, we show accounts receivables as current asset. It means, it is short term loan which is given by organisation to other customer. This loan may be in cash or in stock. So, we have to take money after sometime. That is the reason, we show it in current asset on balance sheet.

For example, A book stores buys the books of Rs. 5,00,000 from B Publishers on the credit. A promises to B after the end of 2nd month. Before the payment from A, B publisher will show A and all other customers who buy from him in asset side of balance sheet with the name of account receivables.

Time to time, bad debts and provision of doubtful debt is deducted from account receivables on same balance sheet. With this, correct amount will be shown which we have to get from our customers.

If we add cash, inventory unsold and other current asset and deduct all current liabilities, it will be equal to working capital which can be shown liabilities side. One is working capital, second is long term debt and third is equity capital. Total of this will be total liabilities. Now, you can understand the importance of account receivable on balance sheet. It is one of important part of balance sheet. Company's policy should be receive its amount as soon as possible. Its increase or decrease will effect on the working capital. As a good businessmen, we should not ignore our customer who buy us on credit. If we will not sell on credit, they can buy from others. With this, there will direct decrease in the working capital because there is no hope of cash from this source. Only to care and proper management of accounts receivable is needed

We company will receive all amount from account receivable on its due date. We will show nil amount of accounts receivables on balance sheet.

For example, A book stores buys the books of Rs. 5,00,000 from B Publishers on the credit. A promises to B after the end of 2nd month. Before the payment from A, B publisher will show A and all other customers who buy from him in asset side of balance sheet with the name of account receivables.

Time to time, bad debts and provision of doubtful debt is deducted from account receivables on same balance sheet. With this, correct amount will be shown which we have to get from our customers.

If we add cash, inventory unsold and other current asset and deduct all current liabilities, it will be equal to working capital which can be shown liabilities side. One is working capital, second is long term debt and third is equity capital. Total of this will be total liabilities. Now, you can understand the importance of account receivable on balance sheet. It is one of important part of balance sheet. Company's policy should be receive its amount as soon as possible. Its increase or decrease will effect on the working capital. As a good businessmen, we should not ignore our customer who buy us on credit. If we will not sell on credit, they can buy from others. With this, there will direct decrease in the working capital because there is no hope of cash from this source. Only to care and proper management of accounts receivable is needed

We company will receive all amount from account receivable on its due date. We will show nil amount of accounts receivables on balance sheet.

No comments:

Post a Comment